The gaming industry is bracing for significant financial pressures as an unprecedented boom cycle in memory and storage demand, largely fueled by the relentless expansion of Artificial Intelligence (AI) infrastructure, drives prices skyward. This surge in costs for DRAM (Dynamic Random-Access Memory) and NAND flash storage, the foundational components for rapid access and long-term data retention respectively, is poised to reverberate across the entire gaming ecosystem, impacting hardware manufacturing, software development, and ultimately, consumer pricing.

The AI Imperative and Its Impact on Memory Markets

The escalating demand for high-performance computing necessary to train and deploy advanced AI models has ignited a supply crunch for memory components. AI workloads, particularly large language models and complex neural networks, require immense quantities of high-bandwidth memory (HBM) and conventional DRAM. This unprecedented enterprise-level appetite has diverted manufacturing capacity and resources, leading to a significant reprioritization by memory suppliers away from the consumer segment.

According to Omdia’s Memory and Storage research teams, the repercussions are already being felt. Mainstream PC DRAM and SSD prices witnessed average increases of nearly 100% and 40% respectively in 2025. This upward trajectory is far from over, with contract pricing continuing its ascent into the first quarter of 2026. Projections indicate a further 60% rise in DRAM prices and a staggering 70% increase for NAND memory during this period. These figures represent a profound shift in component costs, directly challenging the delicate economic models underpinning the production of gaming hardware and software.

Historically, the memory market has been characterized by cyclical boom-and-bust periods. However, the current cycle is distinct due to the scale and sustained nature of AI demand. Unlike previous cycles driven by PC or mobile market surges, AI’s insatiable need for memory is a fundamental, long-term trend, suggesting that a swift reversal of these price increases for consumer products is unlikely in the immediate future. Memory manufacturers are strategically leaning into the enterprise segment, where margins are often higher and demand more consistent, thereby deprioritizing consumer-grade memory supply. While the pace of price increases is expected to cool off somewhat in the second quarter of 2026, suppliers are anticipated to retain significant leverage in negotiations throughout the year, ensuring the upward pressure persists.

Console Hardware Margins Under Extreme Pressure

Dedicated gaming hardware, notably consoles, relies heavily on memory and storage components. Omdia’s analysis from Q2 2025 revealed that the combined memory in a base PlayStation 5 console already accounted for at least 20% of its overall Bill of Materials (BOM). With component prices doubling in some cases, this percentage is set to climb dramatically, squeezing the already razor-thin margins that console manufacturers typically operate with.

Manufacturers usually work through existing inventories of components before new pricing takes effect. Once these stockpiles are depleted, new devices will be built with memory supplies secured at substantially higher contract prices. This applies universally across the console landscape: GDDR6 for the standard PlayStation 5, additional DDR5 for the anticipated PlayStation 5 Pro, and LPDDR5 for the forthcoming Nintendo Switch 2. Each of these memory types is crucial for delivering the performance expected by modern gamers, from high-fidelity graphics to rapid loading times.

The financial vulnerability of console hardware was starkly illustrated in February 2026 when Sony Interactive Entertainment reported increased losses from hardware sales following aggressive discounting of PlayStation 5 consoles during the 2025 holiday season. This situation underscores the precarious balance between maintaining competitive pricing and achieving profitability. With memory costs rising, such aggressive discounting strategies become unsustainable, forcing manufacturers to reconsider their pricing models or absorb significant losses. Industry analysts suggest that major console manufacturers are now in advanced discussions with their supply chain partners, exploring all avenues to mitigate these cost increases, including exploring alternative component sourcing or negotiating longer-term supply agreements, albeit at higher rates.

Mitigation Strategies for Console Manufacturers

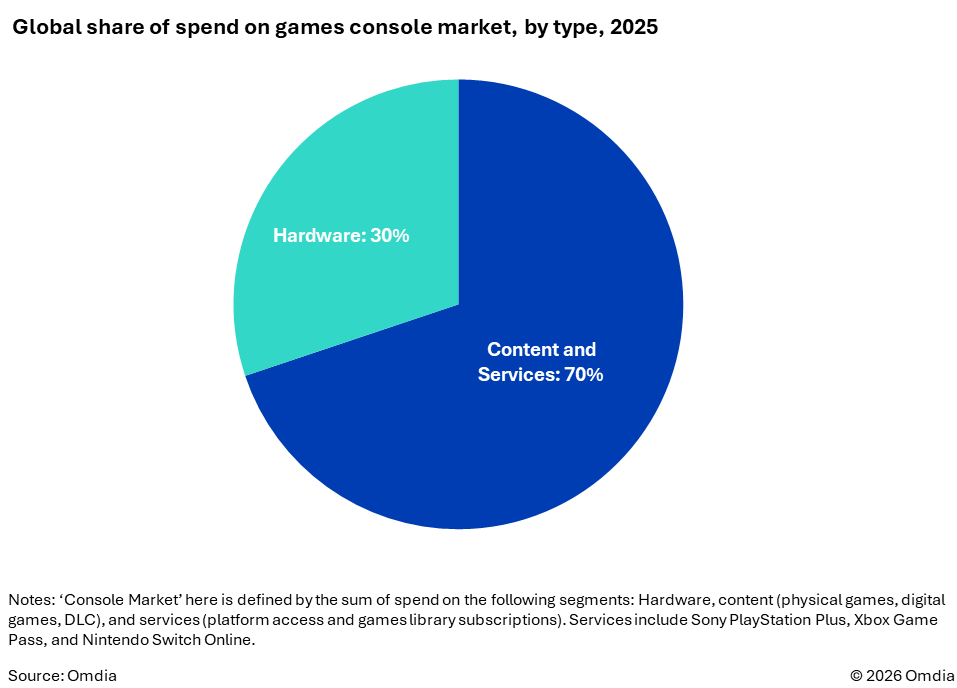

Despite the challenges, console manufacturers possess a distinct advantage over their PC hardware counterparts: robust ecosystems encompassing software, services, and peripherals. These diverse revenue streams offer critical levers to offset squeezed hardware margins. As highlighted in Figure 1 from Omdia, content and services constitute the overwhelming majority (70%) of consumer spending on games console platforms, with hardware making up the remaining 30%. This diversified income stream provides a buffer against fluctuating component costs.

A likely outcome in 2026 is an upward adjustment in the pricing of subscription services. Nintendo, for instance, is expected to increase the cost of its Nintendo Switch Online subscriptions. Omdia estimates indicate that the average selling price (ASP) growth for all Nintendo Switch Online tiers between late 2021 and 2025 was a modest 8%. This contrasts sharply with the 40% growth seen in PlayStation Plus and a substantial 72% for Xbox Game Pass over the same period, suggesting Nintendo has considerable room to maneuver its subscription pricing without alienating its user base, especially given the perceived value of its classic game libraries and online features.

Beyond subscriptions, a broader re-evaluation of pricing for upcoming first-party content and peripherals is anticipated. Game developers and publishers, particularly those tied to console platforms, may need to factor in higher development and distribution costs, potentially leading to increased launch prices for new titles. The eagerly awaited launch of Grand Theft Auto 6 during holiday 2026 could play a crucial role in sustaining demand across platforms, potentially allowing console manufacturers to avoid a repeat of 2025’s deep hardware discounts. The sheer anticipation and projected sales volume of such a marquee title could temporarily insulate the market from some of the inflationary pressures.

Furthermore, the substantial combined active installed base of PlayStation 5 and Xbox Series X/S consoles, now entering their seventh calendar year on the market, offers a degree of stability. These platforms represent a mature market with a large, engaged audience ready to purchase software and services. In contrast, the publishing opportunity on Nintendo platforms appears most exposed. With a vast majority of major new and upcoming first and third-party software transitioning to the nascent Switch 2, the platform’s initial adoption rate and the willingness of consumers to invest in its ecosystem will be critical in determining its resilience against rising costs.

The Erosion of Entry-Level Hardware and Consumer Access

The rising cost of components is particularly detrimental to entry-level hardware in the console market. Historically, last-generation systems or more affordable variants have provided an accessible entry point into a platform’s gaming catalog, nurturing future generations of enthusiasts. The Nintendo Switch, for example, has successfully leveraged its affordability and versatility to attract a broad demographic. However, the price of such entry-level platforms is now likely to rise globally. This trend has already been observed in the North American market, influenced by the introduction of tariffs on imported goods, further exacerbating cost pressures.

This development carries significant long-term implications for market growth and inclusivity. With signs emerging that the spending power of middle-income households is declining in key console markets like the US, the absence of an affordable entry point into a console platform’s ecosystem could severely impact the pipeline of future generations of enthusiast early adopters. A higher barrier to entry risks alienating casual gamers and families, potentially leading to a more segmented and less diverse gaming population. Industry bodies and consumer advocacy groups have expressed concerns about the potential for these price increases to create a widening gap in access to entertainment technology.

PC Gaming: Less Flexibility, New Opportunities

The PC gaming market faces a different set of challenges. Major PC hardware vendors, unlike console manufacturers, do not control the underlying PC games software ecosystems such as Steam. This structural difference means that hardware profitability is paramount for these vendors, leaving them with less "wriggle room" to absorb component cost increases. Consequently, the rise in memory and storage prices is likely to be directly passed on to consumers through higher selling prices for both complete PCs and individual PC components.

This direct price pass-through is expected to significantly affect the PC upgrade cycle. PC gamers, known for their meticulous hardware choices, may delay full system upgrades or defer individual component purchases, such as new RAM modules or SSDs, waiting for more favorable pricing or until their current hardware truly becomes obsolete. Emerging product categories like handheld gaming PCs, which are already premium offerings, may continue to cater exclusively to an enthusiast audience, struggling to achieve broader market penetration due to their elevated price points. For gaming laptops, PC vendors are likely to concentrate their efforts on driving sales of high-end models, where margins are typically higher, in an attempt to maximize revenue amidst constrained supply.

Despite these hardware-centric challenges, the PC gaming software ecosystem remains robust. Developers are somewhat insulated by pre-existing optimization efforts for power-constrained devices like the Nintendo Switch 2, Steam Deck, and Xbox Series S. This experience in optimizing games for lower-spec hardware means that many titles can already run efficiently on a broader range of PC configurations, mitigating the immediate need for constant high-end upgrades.

Moreover, there exists a vast, largely untapped market of gaming-capable laptops. Omdia’s PC Horizon Service reveals that over 90 million such laptops were sold in 2025. The capabilities of built-in processor graphics have dramatically improved in recent years, offering performance that often exceeds the Steam Deck and, at the high end, rivals the Xbox Series S. This presents a significant opportunity for game publishers to broaden their audience by actively addressing this subset of laptop owners who also engage in gaming. Focusing on optimizing titles for integrated graphics and lower-spec discrete GPUs could unlock substantial new revenue streams.

Crucially, the sales volumes and value of PC games content are not expected to be significantly disrupted. The PC platform boasts a huge and healthy audience of installed devices, perfectly positioned to continue purchasing PC games. Omdia estimates that Steam alone had an astounding 321 million yearly active users in 2025, providing a resilient and expansive market for software sales, irrespective of hardware upgrade cycles.

Switch 2 Software Attach Rates and Physical Media Dilemmas

The historical precedent of chip shortages influencing media formats is not new to Nintendo. In the 1980s, rising manufacturing costs for Famicom cartridges directly contributed to the creation of the Famicom Disc System, which utilized a cheaper, proprietary floppy-disc format. This situation is now repeating itself with the Nintendo Switch 2’s physical media. The standard game cards, while robust, are becoming prohibitively expensive to produce at a scale that accommodates publishers’ typical pricing strategies. Like its predecessor, the Switch 2 is anticipated to be a physical-first platform, with Omdia estimating that 57% of Switch 2 games sold in 2025 (including bundled software) were at retail.

In 2026, publishers shipping high-volume software are expected to increasingly opt for "dataless Game-Key Cards." These cards essentially contain a download code rather than the full game data, protecting publisher margins and enabling lower price points at retail, both at launch and subsequently. This strategy helps maintain affordability for consumers but introduces new challenges. The primary exception to this trend will be niche titles targeting highly engaged collectors, an audience generally less sensitive to price. For these games, publishers might explore charging a higher premium to publish the game fully on a physical game card, catering to the collector’s desire for a complete physical artifact.

However, the widespread adoption of Game-Key Cards presents a significant issue for the Switch 2 publishing ecosystem: internal storage limitations. The device is expected to feature only 230GB of usable internal storage, the lowest among any current-generation console. With the cost of expandable SD Express storage also projected to rise, reliance on digital downloads via Game-Key Cards could severely impact software "attach rates" – the number of games purchased per console. Once players accumulate enough large "forever games" (e.g., live-service titles, expansive open-world games) that consume a significant portion of the internal storage, they may be deterred from purchasing more titles without investing in expensive external storage, thus slowing software sales.

Developers Confront Rising Server Costs

Beyond hardware and physical media, the AI boom is directly impacting game developers through escalating server infrastructure costs. As outlined in Omdia’s "2026 Trends to Watch – Games Tech" report, the intense competition for data center capacity from AI companies is making infrastructure costs a top concern for game studio CTOs in 2026. Game companies have already been rapidly increasing their spending on game servers in recent years to support ever more ambitious online experiences and live-service games.

In response to these cost pressures, studios are increasingly experimenting with a combination of bare metal servers and hybrid cloud strategies. Bare metal servers offer dedicated hardware resources without the virtualization overhead of public cloud services, often leading to better performance and more predictable costs for specific workloads. Hybrid strategies, which blend on-premises infrastructure with public cloud resources, allow studios to optimize for cost, performance, and scalability, dynamically shifting workloads to the most cost-effective environment.

Smarter infrastructure strategies are no longer merely an optimization goal but an essential defense against cost increases driven by the memory boom cycle. Developers now have more options than ever, with a growing range of bare metal providers and sophisticated server orchestration solutions. Even hyperscale cloud providers are responding by developing and offering more cost-effective solutions and pricing models tailored to specific gaming workloads, recognizing the long-term potential of the gaming market despite current AI-driven diversions.

Conclusion: A Landscape of Adaptation and Re-evaluation

The current memory boom cycle, primarily driven by the insatiable demands of AI infrastructure, represents a significant and sustained challenge for the gaming industry. While component price increases are expected to cool off somewhat in the second quarter of 2026, memory suppliers are anticipated to maintain their advantage, making a full pricing reversal unlikely throughout the year. This persistent pressure will be an ongoing concern for the launch of specialist products in 2026, such as new iterations of Valve’s Steam Machine or the conceptual Steam Frame, which rely heavily on efficient component sourcing.

The gaming industry has navigated boom and bust cycles in component pricing before. However, previous cycles often occurred during periods of stronger overall market growth, making it easier for companies to absorb or pass on costs. The current climate, marked by broader economic uncertainties and shifting consumer spending habits, presents a more complex challenge.

In 2026, stakeholders across the gaming industry must anticipate and implement strategic adaptations. This includes a comprehensive re-evaluation of pricing across first-party content, peripherals, and services by platform holders. Major PC gaming hardware vendors will likely intensify their focus on high-end models to maximize revenue from constrained supply. Concurrently, game developers will be forced to scrutinize and optimize their server infrastructure strategies to control escalating operational costs. The ability of the industry to innovate in its business models, embrace new distribution methods, and adapt to these fundamental shifts in the supply chain will ultimately determine its resilience and continued growth in an increasingly AI-dominated technological landscape.

Game Developer and Omdia are sibling organizations under Informa.