The global mobile gaming landscape in February continued to exhibit significant shifts in consumer behavior, as highlighted by the latest industry data provided by Appmagic. While the month is traditionally characterized by a shorter reporting window, the performance of top-tier titles reveals a complex interplay between seasonal live operations, regional market dominance, and the evolving preferences of a global player base. Despite a general downward trend in absolute download numbers for some of the market’s most established titles, the industry saw remarkable resilience from puzzle-based applications and a resurgence in the battle royale sector driven by high-profile collaborations and cultural festivities.

Central to the month’s findings is the continued dominance of Block Blast, which secured its position as the most downloaded mobile game globally for another consecutive month. However, the broader market context suggests a cooling period following the holiday surges of late 2024 and early 2025. This report provides a comprehensive examination of the top 20 titles, the regional drivers of growth, and the strategic maneuvers employed by publishers to maintain engagement in an increasingly competitive digital ecosystem.

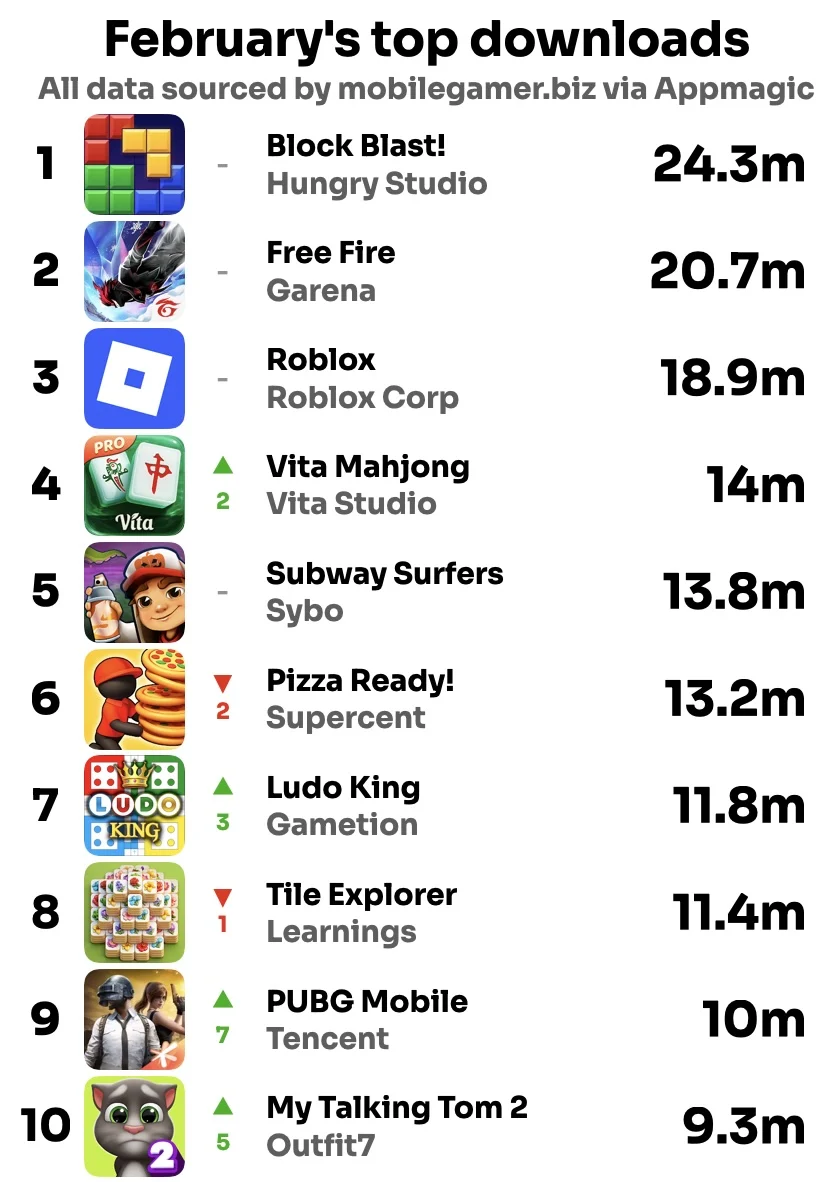

The Puzzle Sector and the Resilience of Block Blast

Retaining its position at the vanguard of the global mobile gaming charts, Block Blast continues to demonstrate the enduring appeal of the puzzle-block subgenre. Developed by Hungry Studio, the title has successfully carved out a niche by offering a refined, accessible experience that appeals to a broad demographic. While the game remained the most downloaded title in February, it experienced its second consecutive month-on-month decline. This follows a record-breaking peak in December, where the title surpassed 38 million installs.

In February, Block Blast generated nearly 4 million more downloads than its nearest competitor, Free Fire. This gap, while significant, indicates a narrowing lead as the title moves from a hyper-growth phase into a period of market stabilization. Industry analysts suggest that the decline is not necessarily a reflection of waning interest but rather a natural correction following aggressive user acquisition campaigns conducted during the final quarter of the previous year. The game’s ability to maintain a lead of several million downloads despite these declines underscores its status as a foundational title in the current mobile market.

Battle Royale Dynamics: Free Fire and PUBG Mobile

The battle royale genre remains a cornerstone of mobile gaming, particularly in emerging markets. Garena’s Free Fire maintained a firm grip on the second-place position, consistently generating over 20 million downloads per month. Free Fire’s success is largely attributed to its optimization for low-to-mid-range hardware, making it the preferred choice for players in Southeast Asia, Latin America, and India. The game’s steady performance suggests a highly loyal user base that is less susceptible to the volatility seen in newer puzzle or hyper-casual titles.

Parallel to Free Fire’s stability, Tencent’s PUBG Mobile witnessed a notable surge in February, climbing seven places in the global rankings. This upward trajectory was fueled by a sophisticated live operations strategy that leveraged major cultural and commercial events. The introduction of Lunar New Year-themed content provided a significant boost in the Asian markets, while Valentine’s Day events catered to a global audience. Furthermore, a high-profile collaboration with luxury automotive brand Ferrari introduced exclusive in-game assets, driving both engagement and new installs. This strategic use of time-limited events highlights the importance of "Live Ops" in sustaining the lifecycle of mature titles in the competitive battle royale space.

Roblox and the UGC Platform Evolution

Roblox, the premier user-generated content (UGC) platform, experienced a unique statistical milestone in February. For the first time since April 2025, the platform’s monthly downloads dipped below the 20 million mark. While a dip below this psychological threshold might initially appear concerning, a year-on-year analysis provides a more positive outlook. In February 2025, Roblox recorded 17.8 million downloads; last month, that figure stood at nearly 19 million.

This year-on-year growth suggests that Roblox is continuing to expand its reach, even as it faces the natural fluctuations of a shorter month and the typical post-holiday slowdown. The platform’s ability to grow its baseline install rate by over a million downloads annually reflects its successful transition from a children’s gaming app to a comprehensive social and creative ecosystem. The dip below 20 million is largely attributed to the "short month" effect, where the 28-day window provides fewer opportunities for aggregate download accumulation compared to the 31 days of January.

Emerging Trends in the Puzzle and Casual Categories

Beyond the top three, the rankings reveal a diversifying puzzle market. Vita Mahjong, which had seen four consecutive months of aggressive growth, saw a slight decrease in total downloads in February. However, due to the relative decline of other titles, it actually ascended two spots in the overall rankings. This indicates that the game’s momentum remains strong, and its performance on a per-day basis likely exceeded that of the previous month.

Relative newcomer Tile Explorer, published by Learnings, continues to display an unpredictable but generally upward trajectory. After a massive spike in July 2025, which saw installs reach 15.6 million, the game experienced a cooling period. However, the first two months of the current year have shown a renewed interest in the title. Adjusting for the shorter duration of February, Tile Explorer’s performance was effectively higher than its January results, suggesting that its refined tile-matching mechanics are resonating with a stable audience.

Meanwhile, the "steady trio" of Subway Surfers, Pizza Ready, and Ludo King continues to occupy the 11 million to 14 million download bracket. These titles have become staples of the mobile gaming diet, showing remarkable consistency over several years. Their performance in February, while lower in absolute numbers than in January, reflects a "business as usual" state, with daily active user (DAU) numbers remaining largely unaffected by seasonal shifts.

Regional Growth Drivers and the Ad-Funded Model

A significant highlight of the February data is the performance of School Party Craft by Candy Room Games. Ranking as the 11th most downloaded game globally, the title has found immense success in specific regional corridors, namely Indonesia, India, Brazil, and Mexico. These markets are currently the primary engines of volume for the mobile gaming industry.

The business model of School Party Craft provides a compelling case study for the "ad-funded" approach. Despite a staggering lifetime download total of 269 million, Appmagic data indicates that the game generates virtually zero revenue from In-App Purchases (IAP). Instead, the publisher relies entirely on advertising revenue. This strategy is particularly effective in regions where credit card penetration is low or where the player base has lower discretionary spending power but high engagement time. The success of School Party Craft demonstrates that massive scale can be achieved and sustained without traditional monetization structures, provided the content aligns with the social and creative interests of younger demographics in emerging economies.

Mid-Tier Rankings and Market Volatility

The 11th through 20th positions in the February rankings show a high degree of volatility, with several titles leapfrogging established names. Notable performances include:

- Solitaire Associations Journey (Hitapps): Despite falling four places to 12th, the game remains a dominant force in the classic card game segment.

- Paper.io 2 (Voodoo): This title also saw a drop of four places, landing at 13th. The decline of "IO" style games often follows a cyclical pattern of viral resurgence followed by stabilization.

- 8 Ball Pool (Miniclip): A perennial favorite, Miniclip’s flagship title continues to hold a spot in the top 20, bolstered by a robust competitive ecosystem.

- Mobile Legends: Bang Bang (Moonton): The MOBA title saw a rise in rankings, benefiting from its massive popularity in Southeast Asia and its growing presence in the global esports scene.

- Candy Crush Saga (King): Remaining at 18th, the veteran title continues to prove that well-maintained legacy games can compete with newer, trendier releases through constant content updates and level expansions.

Several titles that were previously in the top 20, such as Royal Kingdom, Township, and LastWar, saw month-on-month drops, falling behind the rising mid-tier games. This suggests a highly fluid market where the barrier to entry for the top 20 is constantly shifting based on the success of specific marketing bursts or viral social media trends.

Technical Considerations: The Fragmented Android Market

It is important to note that the data provided by Appmagic, while comprehensive, excludes figures from China’s fragmented third-party Android stores. China represents one of the world’s largest mobile gaming markets, and its exclusion means that titles popular in that region—such as Honor of Kings or Peacekeeper Elite—might not appear in these global rankings despite having download volumes that would likely place them in the top five.

Furthermore, the data reflects "unique" downloads, excluding re-installs or updates, providing a clearer picture of new user acquisition. The exclusion of the Chinese Android market remains a standard limitation in Western market analysis due to the lack of transparent, centralized reporting from the various app stores operated by companies like Huawei, Xiaomi, and Tencent.

Broader Impact and Industry Implications

The February download trends suggest an industry in a state of mature stabilization. The era of explosive, unexpected hyper-casual growth appears to be giving way to a more calculated market where "hybrid-casual" games—those that combine simple mechanics with deeper progression systems—hold the most sway.

The rise of titles like Block Blast and Vita Mahjong indicates that the "Silver Gamer" demographic and the "casual commuter" remain the most reliable sources of downloads. Simultaneously, the success of PUBG Mobile and Free Fire proves that the "hardcore" mobile experience is not only viable but essential for maintaining high engagement levels and driving revenue through live events.

As the industry moves into the second quarter, the focus for publishers will likely shift toward retention and the optimization of ad-revenue streams, particularly as privacy regulations continue to complicate traditional user acquisition. The resilience of ad-funded models in emerging markets provides a blueprint for future growth in regions where the traditional IAP model has yet to fully take root.

In conclusion, February’s data reinforces the narrative of a two-speed mobile market: one driven by the massive, consistent volumes of established social and battle royale platforms, and another driven by the rapid, viral cycles of puzzle and casual titles. While the short duration of the month may have suppressed total figures, the underlying health of the mobile gaming ecosystem remains robust, with new contenders regularly challenging the status quo and legacy titles utilizing sophisticated live operations to maintain their relevance.